The Fast Casual Reckoning

Just 12 months ago, Chipotle, Cava, and Sweetgreen were Wall Street darlings—posting stock gains of 150-189% and trading at eye-watering multiples. Cava hit 243x forward P/E. Then reality hit

FINANCEMODELINGINVESTMENT BANKINGVALUATION

Ascendant Training

11/3/20252 min read

I remember when I first came to NYC 25 years ago – it was my first time encountering finance bros and their love of $20 midtown lunches. I found it funny watching everything come and go in cycles: Subway gave way to Quizno’s, which in turn became salad chains, eventually to be replaced by Chipotle and Qdoba, which eventually became Poké bowls. Every fad lasts a few years and feels “fresh” yet it all goes on and on in a cycle (and magically always costs at least $20 😭).

Just 12 months ago, Chipotle, Cava and Sweetgreen were Wall Street darlings—posting stock gains of 150-189% and trading at eye-watering multiples. Cava hit 243x forward P/E. Investors extrapolated double-digit same-store sales growth into perpetuity. Then reality hit.

https://qz.com/restaurant-recession-chipotle-sweetgreen-cava-fast-casual-stocks

What’s changed?

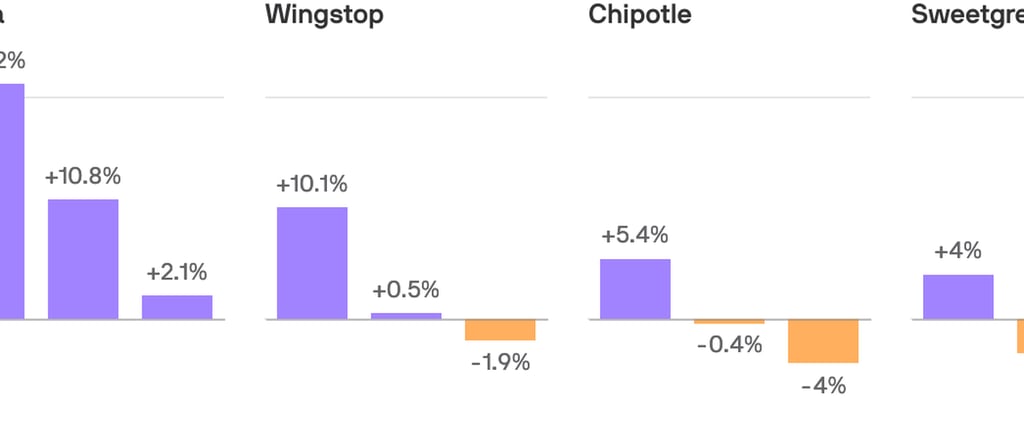

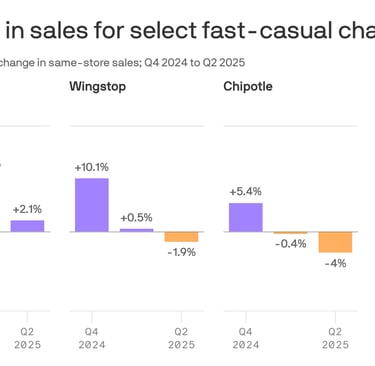

📉 Same-store sales: From +18% growth to -4% to -7.6% YoY declines

💰 Consumer sentiment: The 25-35 white-collar demographic—their core customer—pulled back

🥗 Value perception: $16-20 bowls competing with $5 McDonald's meal deals

📊 Market cap: ~$50 billion evaporated across three companies in 2025

The Finance Lesson:

This isn't just about restaurants—it's a case study in growth rate sensitivity and multiple compression.

When you're trading at 100-240x earnings, you're not buying a company—you're buying a growth trajectory. The market priced these businesses as if exceptional growth was permanent. But in DCF analysis, even small changes to perpetual growth assumptions create massive swings in terminal value (which often represents 60-80% of enterprise value).

Cava's stock fell 16% in a single day when Q2 same-store sales came in at 2.1% vs. expectations of 6%. That's not irrational—it's math. High-multiple stocks exhibit exponential sensitivity to growth deceleration.

The Broader Context:

Fast-casual was supposed to be recession-resistant. These brands offered "affordable premiumization"—better quality than QSR, better value than casual dining. But they hit the ceiling when:

🍎Food-away-from-home inflation outpaced grocery prices

🏢Return-to-office momentum stalled in key urban markets

🍔Value-conscious consumers traded down to QSR deals

What's Next?

These companies are responding with portion increases (Sweetgreen: +25% protein), value menu drops, and automation investments (robotics in kitchens). The question: Can operational improvements restore margin AND traffic?

From a valuation perspective, we're watching a real-time reset. These stocks may find support as multiples compress to more sustainable levels—but only if management can demonstrate stable, mid-single-digit same-store sales growth going forward.

Key Takeaway for Investors & Analysts:

Today's darling at 200x P/E can become tomorrow's sell-off. We're living in a world of high valuations so check those growth rates and assumptions.

👉 Not shopping at Cava or Sweetgreen anymore – what’s your guilty pleasure for lunch?

Where Wall Street comes for Training

CONTACT

MAILING LIST

+1-646-801-6208

© 2025 Ascendant Training LLC. All rights reserved.